If you speak to a financial advisor or anyone who’s read a personal finance blog, you’ll hear the same thing:

“You should always own bonds as well as stocks. Bonds smooth out the performance of your portfolio, because their performance holds up when stocks are doing badly”

This has been true in the past. Not always, but mostly. Owning a 60/40 mix of stocks and bonds would have aided the quality of your sleep during the stock market pull-backs of 2020, 2008, 2000, and further back too.

(“Bonds” can refer to debt issued by a company or a government, but in this context people are usually talking about government bonds – so whenever you read “bonds” in this article, that’s what I mean.)

A proper personal finance blogger would show you a graph of extensively back-tested data at this point. But I’m not a proper personal finance blogger, so you’ll just have to take my word for it and look at a picture of Billy Bonds (799 appearances for West Ham United between 1967 and 1988) instead.

Anyway. Whatever was true in the past doesn’t matter, because it can’t possibly be true in the future.

The reason is obvious.

When interest rates go up (or there’s an expectation of interest rates going up), bond prices go down.

Why? Because:

- A bond pays a fixed return every year

- When interest rates increase, that fixed return suddenly seems less attractive compared to other investments.

- So to make it match other investments in attractiveness, you’ll now need to offer a discount to entice someone to buy that bond from you.

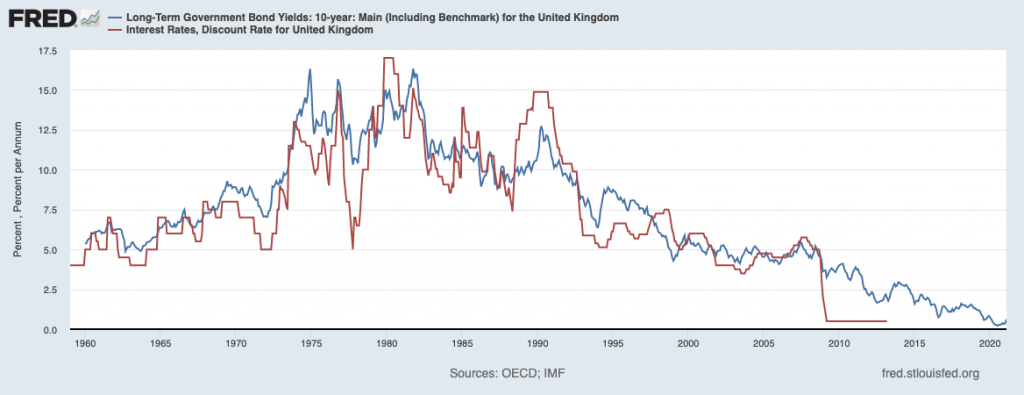

Brace yourself: here comes a proper graph to prove it

What you see here is:

- In red, the interest rate – or more accurately, the Bank of England base rate. (For some reason on my graph it konks out in 2013, but after that it stayed roughly where it was before falling to 0.1% in 2020)

- In blue, the yield on 10 year UK government bonds

There’s one thing you need to know about bonds to understand this: the yield going up means the price going down, and vice versa. This is an iron-clad law.

So when the red line is falling, that means bonds are getting more expensive.

What do you observe from this graph?

Hopefully, it will have struck you that the two lines follow each other pretty closely.

It’s not a perfect relationship, but what relationship is perfect really? In any event, it’s close enough: if someone was following me that closely I’d be clutching my bag more tightly and desperately trying to remember a move from that one Krav Maga class I went to once.

- Interest rates were on an up-trend from 1960 to 1980, and have been on a down-trend ever since – finally reaching basically zero in 2020.

- Bond prices were mostly falling between 1960 and 1980, and have been rising ever since.

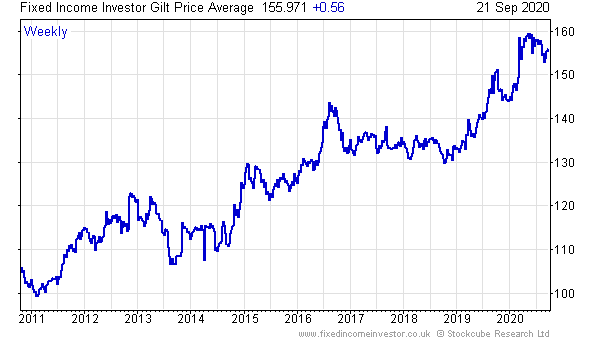

I know: it’s confusing because we’re looking at bond yields, so “going up” means the line is going down. Here’s a chart showing bond prices going up over the last decade, which looks a bit more intuitive:

So…where from here, do you think?

For bond prices to go anywhere but sideways or downwards from here, one of two things needs to happen.

Option 1: Interest rates fall. As in, fall from their current 0.1%. It’s possible, but it’s like rolling a 2 on a 12-sided die and being asked to bet on if the next roll will be higher or lower. Betting “lower” isn’t always going to be a losing proposition, but the odds aren’t with you.

Option 2: The creditworthiness of the UK government improves from where it is now, so people are even more happy to lend it money at a given rate of return. To which the only sensible reaction is:

I’m not saying the UK is going to default on its debts. I’m just saying when government bonds are considered the “risk-free” asset against which everything else is compared, there’s only one way to go.

Let’s think through what the next crisis is likely to look like.

Historically, when the economy has hit a rough point:

- The government reduces interest rates to stimulate the economy

- This is good for bonds, as discussed

- This is bad for stocks (and in any case, people are less keen on holding “risk assets” so stocks sell off)

Voila – bonds go up, stocks go down, so holding a mix of both gives you a better result than stocks alone.

Next time though, things are likely to be different:

- The government can’t reduce interest rates, because they’re already at rock bottom

- Instead, they borrow and print a bunch of money to help the economy out

- If anything this is bad for bonds, because it creates questions about the government’s creditworthiness

Result? I’m not suggesting bond prices would crash immediately (they almost certainly wouldn’t), but at some point there’s a whole load of downside risk waiting to hit you.

And I haven’t even mentioned…

…that the returns currently offered by bonds are lower than the rate of inflation.

This means that a year after lending the government £100, you might get paid 70p – but in the meantime the purchasing power of your £100 has fallen to £99. Repeat every year.

Sure, a steady dripping away of your wealth is preferable to a sudden crash in the stock market…but less preferable than almost anything else you could invest in.

With property, you can earn a positive (and inflation-linked) return, with the possibility of using debt that’s constantly devaluing.

With gold, there’s a natural scarcity and no credit risk.

And let’s not even mention Bitcoin…

Here’s what an honest sales pitch for bonds would look like:

- Lend me money, and I’ll eventually pay you back with money that’s worth less (after inflation) than you gave me

- By the way, I’m printing as many of these bonds as people will buy, and selling them to whoever wants them – there’s no scarcity whatsoever

- Because I’ve flooded the market with these already, if sentiment shifts and suddenly there are more sellers than buyers, we have big problems

- But hey, worst comes to worst we’ll just print a load of new money to pay you back with – which probably won’t have any negative consequences at all…

Are you in?

I’m not. Granted, I’m just a random guy with no particular qualifications so you shouldn’t listen to me. But Ray Dalio agrees with me, so there might be something to it.