Property investment is a complex business – to the extent I’ve written three full books about it (with very little filler, I promise). But when you look at property from a 60,000-foot view, the investment case is so simple it can be summed up in three sentences.

Here they are:

The value of a property priced in pounds will increase as the number of pounds in existence increases. The value of mortgage debt held in pounds will fall as the number of pounds in existence increases. Meanwhile, your rental income stream will generally grow in line with wages.

Let’s explain each of those a little more…

The value of a property priced in pounds will increase as the number of pounds in existence increases

This is the effect of inflation: inflation of the money supply (creating more pounds) leads to inflating prices.

The relationship isn’t perfect because there are many other factors at play, but it holds as a general rule.

Why? Because when you think about it there’s only so much “stuff” in the world: creating extra money doesn’t create any more stuff, and just means you need to use more units of money to represent the stuff you already have.

It’s analogy time…

Imagine that you and three friends have one pizza, and you each have one coin to represent your right to your share of the pizza. One quarter of the pizza is therefore represented by one coin. If one of your friends wanted your quarter of the pizza, they’d give you one coin in exchange for it. For the purpose of this analogy, nothing else exists in your little economy other than the one pizza and four coins: it’s a completely closed system.

Now, imagine someone else comes into your economy and brings another four coins with them. There are now twice as many coins…but still only one pizza. With four slices of pizza and eight coins, would you still sell a slice for one coin? Hell no! Now, if someone wanted to buy your quarter of the pizza, you’d want two coins in exchange for it – because two coins represents a quarter of all the coins in your economy. That’s inflation.

OK, this is just making me hungry so let’s come back to property. There’s only so much property in the UK (the equivalent of the pizza), so if more pounds are printed it’ll increase the number of pounds someone will need to pay for each individual house. Again, in reality there are other factors in play so this won’t play out perfectly at all times, but the general rule holds.

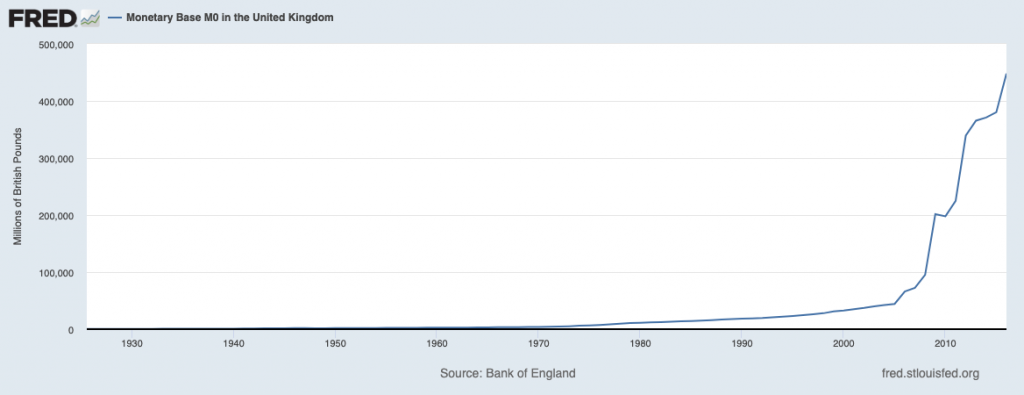

So is the number of pounds increasing? Let’s see…

Yes. Yes it is.

The value of mortgage debt held in pounds will fall as the number of pounds in existence increases

Meanwhile, if you use a mortgage to buy property, you have to pay back a fixed number of pounds at some future date.

To revive my struggling pizza analogy, imagine you’d borrowed the coin that you originally used to claim your quarter of the pizza. Again, the number of coins in the economy then doubles – so your quarter of the pizza is now worth two coins.

You still only owe one coin, even though the “pizza purchasing power” of that coin is now half what it was. As a result, you could pay back the coin you owed, and still own one-eighth of the pizza completely debt-free.

OK, I promise I won’t mention pizza again from this point forward. But this is how mortgage debt works: each pound consistently becomes worth less over time, yet you still only have to pay back the number of pounds you originally borrowed.

It’s easiest to appreciate this over a long timeframe where the effect is exaggerated. For example, if you borrowed £20 in 1920 you could’ve used it to pay your rent for a month and still have enough left over to go out for a nice meal. If you then had to pay it back in 2020, you could just fish a £20 note out of your wallet and hand it over while barely noticing it had gone. That £20 wouldn’t even buy you the meal, let alone the month’s rent.

Meanwhile, your rental income stream will grow in line with wages.

Over the long term, rents tend to rise in line with wages – and wages tend to rise in line with inflation.

To understand this, imagine a static situation with 10 people and 9 houses – some of which are more desirable than others. The poorest two people will compete with each other for the least desirable house, until it reaches a price one of them can’t afford and they remain stuck living with their parents (or in a room in a house-share, or whatever). The next person will be willing to pay a bit more for the next nicest house, and so on – all the way up to the best.

Now, everyone’s wages go up by 2%. The poorest person can now afford to escape from their parents and pay the rent for the cheapest house…but the person already living there doesn’t want to give it up, so they offer to pay the landlord more. The landlord of the next best house now realises that they’re under-charging, so they increase the rent – all the way up to the most expensive.

(This actually still all works in a situation where there’s not a housing shortage, but it’s easiest to understand this way.)

This happens to be an illustration of how land values end up capturing all economic surplus, but for our purposes the point is rising wages mean rising rents. This means your rental income stream is always growing.

In summary…

…property (especially bought with a mortgage) will be a good investment over the long term as long as you believe there will be inflation.

(A quick bunch of caveats: there will be good and bad times to buy, prices don’t neatly track inflation so there will be crashes, when prices fall leverage will magnify losses, changes to the tax regime may make property less attractive, new legislation can make it less appealing, may cause drowsiness, consult with your physician…there are more, but you get the general idea.)

Will there always be inflation? Perhaps not always: the world is inherently deflationary. But given that it’s the policy of every government to produce annual inflation and they’re resorting to ever more exotic methods of achieving it, it seems reasonable to assume it’ll continue until they’ve exhausted every possible tool they have.

So there you go: the whole rationale for property investment, neatly summed up in three sentences. Now, where can I get some pizza…